Attachments to this letter.

#1 The NYS Health insurance Consumer helpline cul du sac

In an attempt to resolve problems with my health insurance I contacted a circuit of government agencies in vain last December. Here is a summary of that healthcare consumer help cul du sac:

The NYS Department of Financial Services helpline (from dfs.ny.gov) referred me initially to the US Department of Health and Human Services (877-696-6775) which, supposedly, connected me to NYS Health and Human Services, although to an incorrect branch of that agency, the pertinent branch apparently having been merged into the NYS Department of Financial Services which took over all functions of the former NYS Insurance Department as well as oversight of banking and several other discrete and seemingly unrelated areas. (When I called this number today, it gave me an option, unavailable last time, to press 6 for “consumer problems with the ACA”, and offered a call back in five business days from a representative.)

The New York State Insurance Department, along with other agencies related to healthcare in New York State, was merged into the Department of Financial Services when New York adopted the Patient Protection and Affordable Care Act (“PPACA”). The New York State Department of Financial Services, it turns out, does not hear consumer fraud complaints against health insurance companies.

I entered this administrative cul du sac in December 2016 after Empire Blue Cross “Health Plus” sent me to two in-network providers for needed medical services, a cardiologist (for follow-up care after a hospitalization for cardiac issues) and a physical therapy facility. Neither provided me with any service.

The fraud investigator I eventually spoke to at the NYS Department of Financial Services, at the end of a long chain of calls, could not find a word other than ‘fraud’ to describe the facts I set forth, but urged me to call the NY State Department of Financial Services Consumer Services Hotline. He assured me that they were the specialists in the area of health insurance. The recorded menu at the hotline, which I recognized from my first call hours earlier, offers no option for resolving issues with insurance companies of any kind.

On my original call to the Department of Financial Services, a long wait to speak to a representative yielded the number of the proper federal agency to contact. Calls to the U.S Department of Health and Human Services are robotically routed to a NY State number that is, sadly, the office of Temporary and Disability Assistance, where a helpful party connects you to a fraud hotline, which turns out to be at the office of the Medicaid Inspector General, where the office of legal affairs is also sympathetic, but unable to help, and so forth.

#2 Permissible grounds for routine denials of purchased healthcare benefits in NYS and limited “appeal” of denials available to New Yorkers

More ominous than the many billing irregularities consumers are left to resolve with the billing parties, a patient can be denied needed medical service without explanation. Permissible corporate reasons for denying service are things like incorrect site-specific provider NPI number and improper CPT pre-authorization codes. These valid grounds for denial are unrelated to an individual consumer’s MOOP, which comes into play more for billing. There is nobody in New York State a patient can appeal these denials of service to, except to the insurance company itself.

Immediately before I was diagnosed with a serious kidney disease, in January 2017, I attempted to resolve some issues I’d been having with my then insurance provider, Empire Blue Cross. This was before I switched to Healthfirst, which has a series of nephrologists I’d been referred to, listed as ‘in network” who, it turned out, were not. Here is the slightly overwrought grievance I wrote when I was a customer of Anthem/Empire. It reflects the frustration of someone caught in this ‘regulatory’ vacuum:

Grievances – Anthem/Empire Blue Cross Blue Shield “Health Plus”

Grievance 1: lack of internal complaint procedure for aggrieved customers

After being chided by an Empire representative for never filing a written complaint about any of the grievances detailed below, I attempted to do so on-line. Logged in automatically under my former bronze plan ID there was an on-line complaint form, easily located. I was unable to update my member ID info. A web support representative at Empire walked me through changing the new log-in. On the website for the “Essential” plan there is no complaint form.

I was also told by web-support/claims representative Laurisha that there is no internal mailing address for submitting a written complaint to Empire and that company policy was not to divulge the name or contact information of company executives. The rep told me she could take my complaint orally over the phone. I decided to try my luck with the original claims person I’d just spoken to for an hour. Nobody was able to connect me to her.

Someone at claims found this answer for me, while looking for the physical mailing address to send a complaint directly to Anthem/Empire. He told me it was printed in red, as I will reproduce it here:

Essential Plan members do not have a right to file complaint appeal (sic). If they need assistance filing a grievance or appeal, they may also contact the state independent consumer assistance program at: Community Health Advocates, 105 E. 22nd Street, NY NY 10010 or 888-614-5400 or email at cha@cssny.org

source: Anthem’s National Contact Center Document under NY market tab for “Essential” plan updated as of 12-14-16 at 7:56 a.m.

Grievance 2: unresolvable bill

8/17/16 I went to Madison Avenue Radiology for an x-ray and two sonograms. I had referrals for all of them. I got a bill from Madison Avenue for $1,324 for one of the sonograms.

On 10/19/16 I spoke to a representative at Empire who spoke to the provider, to a person she told me was named Daniel. I then spoke to Daniel who agreed the $1,342 had been billed in error and told me I’d receive a corrected invoice for the $25 co-pay.

The next invoice I had, in December, was a third notice from Madison Avenue Radiology that I owed $1,342. This time Ty at Empire told me she called the provider, who denied ever speaking with me, and that I owed the entire amount, for reasons I could find in the Essential Plan handbook she offered to send me. She herself did not know the reason a kidney sonogram was covered and a pelvic sonogram was not. She told me I was responsible to pay the $1,342. When I asked to speak to a supervisor she told me no supervisor was available.

(Months later this bill was eventually reduced to a $25 copay)

Grievance 3: fraudulent referral to cardiologist

I was referred, by Empire, to a cardiologist named David Sahar. I was given his site-specific NPI number to see him at his 3050 Corlear Avenue office, I sent front and back of my insurance card to his receptionist who confirmed that we were good to go for a December 15 follow-up to my November 18 Emergency Room visit/hospitalization. Ten minutes into the consultation the nurse who was interviewing me was called away and when she returned she told me Empire had refused to cover the visit. The doctor explained he could not risk not being paid by Empire.

Grievance 4: fraudulent referral to physical therapy

I was referred by Empire to a facility to continue the Physical Therapy I had begun on 11/1/16 at a facility that treated me once and then informed me that they do not accept the Empire Essential Plan. I made several calls to Empire to find out how to get them in network, as Empire told me they could enroll by calling 800-454-3730. After a few weeks calling the PT facility and Empire I gave up. I requested an in-network PT provider and Empire sent me to an address that turned out to be a nursing home. It did not offer PT to outpatients.

Grievance 5: incorrect information; false promises of help from customer service

I called on 12/30/16 in an attempt to resolve these issues, the bill and the two denials of coverage from providers I’d been referred to by Empire. I was told by Joan that the “service not covered” code came up at the cardiologist’s because, likely, an incorrect CPT number had been called in, or possibly the doctor’s office had failed to obtain a prior authorization from Empire’s medical management office, both the fault of the doctor’s office. Empire, I was told, had done nothing wrong. Joan had no explanation for why I was sent to a nursing home for PT or why the kidney sonogram had been covered and the other one not covered. She offered to send me the handbook so that I could read it and find out for myself why one body part is covered and another is exempt from coverage for the same diagnostic procedure.

Joan transferred me to someone who said she was a supervisor. She identified herself as Julie, at the New York Call Center, assured me she was the only Julie there and that I’d have no trouble finding her. She noted that I’d never filed a formal complaint about any of these issues and promised to research and get back to me with the answers on Tuesday, 1/3/17 when the office reopened. Regarding the PT, she gave me a number for a third party vendor called Orthonet. She incorrectly informed me that they could answer any and all PT-related questions. When I called Orthonet the receptionist there told me Orthonet’s only role is to authorize services for PT once a provider makes a request to treat a patient.

When I got no call from Julie at the NY Call Center I attempted to reach her. Ashanti D, user ID AF09740, was very helpful, even giving me the conversation reference number I52146704. She told me that without a last initial or employee ID number it would be impossible to look Julie up. The NY Call Center could not be reached directly by Empire customers, it was an internal number and Ashanti looked it up and transferred me to it. After a long hold the phone rang three times, then the line went dead.

Grievance 6: improper billing practices

I received confirmation of my payment for December and January two weeks before this arrived:

Grievance 7: instead of promised return call, customer service survey

Attempted Customer Happiness surveys asking about each of these “customer service” experiences, by telephone and email.

To show that the corporation is not without a certain sardonic sense of humor, I had a solicitation call from an Empire representative, on 1/4/17, thanking me for my business and offering her assistance in renewing me with Empire so there would be no interruption of insurance for my health care.

#3 The New York State of Health Marketplace

Errors are not easy to resolve at the New York State of Health (”NYSOH”). Answers to routine questions vary from representative to representative. There is a wait of several months to have even the most simple mathematical mistake by the NYSOH corrected, and one must go through a quasi-legal appeal process before NYSOH will correct its error. Attached is a recent decision by a hearing officer that ordered NYSOH to correct an easily detectable mathematical error they had committed months earlier.

Note that any employee of NYSOH could have used the online calculator on their website to instantly verify their error, generated automatically by their website (it is easy to instantly lose insurance coverage at NYSOH, hard to regain it), a mistake that took months to have corrected and resulted in the customer being forced to overpay by almost 100% until they did.

Compounding the aggravation of resolving problems with NYSOH is the policy of its director, Donna Frescatore. Representatives are specifically instructed not to divulge the director’s identity or any way of reaching her office. I have confirmed this policy many times, with many different NYSOH representatives.

#4 Common healthcare billing irregularities in New York State

The PPACA, whose primary drafter, Liz Fowler, went back to work in the health industry after her legislative work was done, apparently contains no provision that the cost of a medical service must be divulged to the patient before the medical service is performed.

The doctor’s office or hospital cannot tell you the fee until the insurance company sends them a statement. The insurance company cannot predict the fee until they get the provider’s bill. The insurance company then eventually sends the patient an Explanation of Benefits, (“EOB”), detailing all charges, payments made and the patient’s responsibility for whatever part of the negotiated rate insurance has not paid. It is like eating at a restaurant with no prices on the menu, and being sent a bill for the meal weeks later. Except, of course, that it is not a meal at a restaurant, it is often a matter of life or death, or, at least, of health-related stress.

My kidney biopsy, for example, may cost the patient anywhere between zero and many thousands of dollars. Simply no way to determine the cost prior to delivery of the service, under current law. I had the procedure on May 26, I got the most recent EOB related to the procedure on September 28. In the intervening four months, I got many bills from the hospital.

Though there is probably nothing your office can do about this particular practice, I offer it as an illustration of the scope of the challenges facing New York healthcare consumers. I provide the following letter to the CEO of Healthfirst as a snapshot of the general billing madness under our current ‘regulatory’ scheme.

Pat Wang

CEO

Healthfirst

100 Church Street

New York, NY 10007

September 26, 2017

Dr. Ms. Wang:

I appreciate that you allow your reps to give out your contact information to customers who can’t otherwise resolve issues with your staff. This encourages me to think that you might be helpful in resolving an aggravating billing situation that has been ongoing for months. I applaud your willingness to be contacted, it shows integrity and is in stark contrast to the policy of Donna Frescatore, director of the “New York State of Health” (NYSOH) ordering her reps not to divulge her name to callers.

I request a corrected bill and an accounting showing my remaining credit toward premium payments. The credit situation is described below.

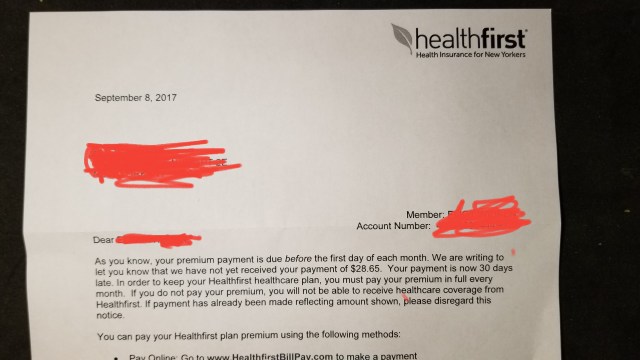

During an August 25th call to Healthfirst to try to resolve the issue of incorrect bills being sent to me, my “case” was assigned an “escalation number” (347-79-923). I was promised an accounting, showing payment history and current credit toward future premiums. I received instead a notice, dated September 8 and signed by Christopher A. DiMarco, threatening me with cancellation of my health insurance for a claimed past due balance of $28.

On September 19 I called Healthfirst and was assured that credit had been applied and my September premium paid in full. I was also informed during that call that “finance” had included no notes on my account. I could not be sent a simple receipt for payment or anything indicating my remaining credit. I was assured by an extremely sympathetic rep that my account was paid through October, with credit remaining toward November’s premium.

Attached is the invoice I received on September 25. It seeks payment of $482 for October (plus a past due amount), nonpayment of which will result in losing my health insurance (as I begin treatments for kidney disease and skin cancer). It has been mailed to me in error. I have a credit of several hundred dollars due to overpayments made as a result of NYSOH’s error. NYSOH incorrectly denied my subsidy for 2017. It took months, and a ruling by a hearing officer, before NYSOH was ordered to retroactively restore the subsidy, about fifty percent of the premium.

As a result of NYSOH’s error, I was required to pay Healthfirst the full premium from February through June. When I got a bill for July, I called Healthfirst and learned that a credit had been applied for my overpayment. After payment of July’s premium the rep calculated my remaining credit at $876.

Since then it has been a health insurance headache every month. In another context, it would be tempting to characterize the attached invoice demanding payment for a premium I have already paid as an attempt at fraud. I am sure it was sent to me in error. Please have somebody update my account and send me an accurate statement of my payments and remaining credit.

(invoice attached here)

Thanks,

A short time later, after a call from one of Ms. Wang’s assistants, I got a corrected bill that demanded payment of -$183 on or before October 1.